March 24, 2015

Starting the Conversation

“The secret is … it’s just not that hard.”

What are we talking about? The discussion about money and retirement. So if it’s not that hard, what’s stopping the majority of women from talking about their finances and financial futures? Perhaps it’s a lack of confidence. Or a lack of time. Or simply not knowing where to start. Whatever it is that’s causing the foot dragging, it affects the majority of women. And that simply means the conversation is not taking place at all. Which is a serious issue as women have greater retirement needs; they live longer than men and often have to make up for lost years when they take time out to raise a family.

What to do? Start by talking. Begin the conversation. Learn. Educate yourself. Take charge.

For more on the topic, check out this smart article from Fidelity here. Questions? Of course call or email us. We love talking financial strategy and creating road maps toward strong financial futures.

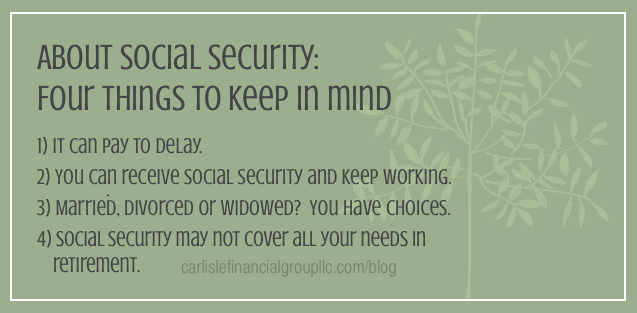

Part of a smart investment/retirement strategy includes how and when you’re going to use your social security. When it comes to social security, there are four basic elements to consider:

Part of a smart investment/retirement strategy includes how and when you’re going to use your social security. When it comes to social security, there are four basic elements to consider: